![]() Securities class action litigation activity involving IPO companies recently has been a significant concern, for the companies themselves as well as for their insurers. In the following guest post, Stanford Law School Professor Michael Klausner and Jason Hegland, Stone Kalisa, and Sam Curry of Stanford Securities Litigation Analytics take a look at the data surrounding IPO-related securities litigation. I would like to thank the authors for allowing me to publish their article as a guest post on this site. I welcome guest post submissions from responsible authors on topics of interest to this blog’s readers. Please contact me directly if you would like to submit a guest post. Here is the authors’ article.

Securities class action litigation activity involving IPO companies recently has been a significant concern, for the companies themselves as well as for their insurers. In the following guest post, Stanford Law School Professor Michael Klausner and Jason Hegland, Stone Kalisa, and Sam Curry of Stanford Securities Litigation Analytics take a look at the data surrounding IPO-related securities litigation. I would like to thank the authors for allowing me to publish their article as a guest post on this site. I welcome guest post submissions from responsible authors on topics of interest to this blog’s readers. Please contact me directly if you would like to submit a guest post. Here is the authors’ article.

************************

In recent years, commentators have expressed concern regarding litigation risk associated with going public—specifically, that IPOs are more likely to become the object of securities class actions than they were in the past.[1] In this post, we use data from the Stanford Securities Litigation Analytics (SSLA) database to investigate the extent and the nature of this reported surge in IPO-related litigation. Specifically, we analyze the volume and outcomes of securities class actions that target IPOs from 2010 to 2019.[2] We then compare those data to data on securities class actions based on Section 10(b) of the Securities Exchange Act against already-public companies. We find that, in fact, there has been an increase in litigation targeting IPOs.

Our approach is to establish a direct link between an IPO and a securities class action. This is different from simply counting IPO-related cases each year or counting IPO-related cases in a given year compared to the number of IPOs in that year. Those approaches are flawed because most IPO-related cases are not filed in the year of the IPO. Under Sections 11 and 12 of the Securities Act, which authorize suits based on misstatements and omissions related to public offerings, there is a three-year statute of limitations. Consequently, a high volume of IPOs in a given year or two can result in a high volume of IPO-related litigation over the next few years even if the risk of litigation remains unchanged.[3] Furthermore, under the damage rule applicable to Section 11 and 12 suits, a falling market can result in an increase in IPO-related litigation, and vice versa in a rising market. We take account of this as well.

A second aspect of our approach is to count the number of IPOs that have been targeted by litigation, rather than counting the number of lawsuits filed. As we have documented elsewhere, since the Supreme Court’s early 2018 decision in Cyan, Inc. v. Beaver County Employees Retirement Fund,[4] plaintiffs’ attorneys have frequently filed parallel state and federal cases targeting the same IPO.[5] Commentary to date on increasing IPO litigation seems to have treated parallel pairs of cases as two separate cases.[6] So it is not surprising that, since Cyan, there appears to be a dramatic increase in IPO-related litigation.[7] We avoid this distortion by counting a parallel pair of state and federal cases based on the same IPO as one case, not two.

I. IPO-Related Securities Class Actions Since 2010

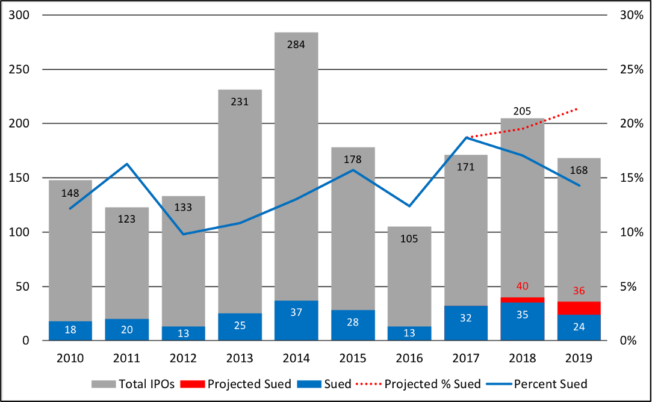

From 2010 to 2019, 14% of IPOs became the target of litigation. Figure 1 graphs the number of IPOs for each year between 2010 and 2019, the number of lawsuits targeting each year’s IPOs, and the percentage of IPOs targeted by lawsuits. To be clear, lawsuits identified as being tied to, say, 2010 IPOs were not necessarily filed in 2010. In fact, most were not. Lawsuits related to 2010 IPOs were filed within the three-year statute of limitations following a 2010 IPO. For 2018 and 2019 IPOs, the statute of limitations has not run. We therefore project lawsuits for those years’ IPOs based on the number of suits filed to date and the historic distribution of lawsuits one, two and three years following an IPO.[8]

Figure 1: IPOs and IPO-Related Lawsuits

Figure 1 shows a gradual upward trend in the percentage of IPOs targeted by lawsuits from 2012 to 2017. That trend continues through 2019 if our projections turn out to be correct. Fourteen percent of 2019 IPOs (24 of 168) had attracted lawsuits with one to two years remaining under the statute of limitations. Based on past experience, we project that lawsuits will target 21% of 2019 IPOs.[9] If 2018 and 2019 projections are borne out, there will be a significant increase in IPO litigation since 2017 and a steeper trend from 10% in 2012 to 21% in 2019. Whether these projections are borne out, however, remains to be seen.

Damages payable under Section 11 and 12 of the Securities Act are measured by the difference between a company’s share price at the time of its IPO and the share price at the time a lawsuit is filed.[10] So, a change in the volume of IPO litigation could result from a rising or falling IPO market, as opposed to a difference in plaintiffs’ lawyers’ practices with respect to filing cases (or the extent to which IPO prospectuses actually contain misstatements or omissions).

In Figure 2, we replicate Figure 1 using only companies whose share price fell 20% or more within three years following their IPO. Because we cannot project how many companies with 2018 or 2019 IPOs will see their share price drop 20% during the three-year statute of limitations following their IPO, we limit Figure 2 to 2010 to 2017. With this limitation to companies with 20% stock drops, the percentage of IPOs facing litigation shows an upward trend since 2013. (The trend is the same for threshold declines of 10% or 30%.)

Figure 2: IPO-Related Lawsuits Against Companies Whose Stock Dipped 20% Below IPO Price

II. Comparison with Section 10(b) Suits

In order to place IPO litigation in context, we compare it to the rate at which already-public companies face securities class actions under Section 10(b) of the Securities and Exchange Act. Between 2010 and 2019, there was an average of about 3,700 companies[11] listed on the NASDAQ and NYSE in any given quarter. During that time, on average and excluding companies that went public in the prior three years, 122 companies[12] were sued per year. So, in any given year, the risk of being sued for an alleged misstatement or omission other than one associated with a public offering is 3.3%, substantially lower than the risk facing companies going public.

We now refine this comparison in two ways. First, to maintain reasonable comparability with IPOs, we limit our comparison to public companies with market capitalization that fall between the first and third quartile of market capitalization among IPOs—between $169.4 million and $978.4 million. Second, we limit the analysis to IPOs that dipped at least 20% below their IPO price, as we did in Figure 2, and to already-public companies that experienced a single-day stock drop of 20% or more.[13] This makes for a somewhat apples-to-apples comparison of companies that, from a potential damages point of view, would be attractive litigation targets. To the extent a 20% single-day stock drop may reflect a corrective disclosure of an actual prior misstatement, however, this comparison would inflate the incidence of Section 10(b) suits and understate the difference between the incidence of IPO litigation and Section 10(b) litigation. That is, a post-IPO share price drop of 20% is probably less likely to indicate that a securities violation may have occurred than a 20% one-day drop in the share price of a mature company.

Once again, due to constraints in projecting IPO lawsuits, we limit this portion of the analysis to 2010-17. Between 2010 and 2017 there were 884 already-public companies with a market cap between $169.4 million and $978.4 million that experienced a stock drop of 20% or more. Among those companies, 13% became the subject of Section 10(b) litigation in connection with one or more of those drops.[14] Over the same time period, there were 1,188 companies that went public and saw their share price dip 20% or more below their IPO prices within three years. Of those, 18% were targeted with lawsuits based on misstatements or omissions related to their IPO. Thus, even with this comparison that overstates the incidence of Section 10(b) litigation, IPOs attract lawsuits at a significantly higher rate than already-public companies.

III. Outcomes of Lawsuits

One reason IPOs entail relatively high litigation risk is that companies are strictly liable for misstatements and omissions under Section 11 and 12 whereas Section 10(b) requires proof of scienter. One would expect, therefore, that Section 11 and 12 suits based on IPOs are dismissed less frequently than Section 10(b) cases. This is indeed borne out in the data. Among cases filed between 2010 and 2019, 39% of IPO cases are dismissed, compared to 56% of Section 10(b) cases against already-public companies. As shown in Figure 3, the dismissal rate for both IPO cases and Section 10(b) cases has risen over time, with IPO dismissal rates notably seeing a much more substantial increase.

Figure 3: IPO vs. Section 10(b) Dismissal Rates

The lower standard of proof in IPO suits is also evident when comparing alleged damages and recoveries.[15] When proposing a settlement to a court for approval, the plaintiffs’ attorney typically provides the court with an estimate of damages incurred by shareholders. Those estimated damages are typically smaller in Section 10(b) cases than in Section 11 and 12 cases, with median estimates of $45.1 million compared to about $53 million, respectively. Section 11 and 12 cases then ultimately settle for higher dollar-amount settlements and significantly higher recovery percentages. Settled IPO cases had a median settlement of $8 million and median recovery of 16%, compared to $5.5 million and 12.6% for Section 10(b) cases.

IV. Conclusion

There has been an upward trend in the litigation risk associated with IPOs. This increase cannot be traced to Cyan or falling market prices. Furthermore, the incidence of litigation for firms going public is substantially greater than the incidence of Section 10(b) litigation for more mature companies. Case outcomes are less favorable for defendants in IPO cases than in Section 10(b) cases, as well. IPO cases settle more often and are dismissed less often than Section 10(b) cases, and controlling for company size, they typically settle for larger amounts and larger percentages of plaintiffs’ estimated damages. In sum, the litigation landscape for companies going public is more treacherous than it is for mature companies, and that situation appears to have gotten worse over the past several years.

____________________________________

[1] Rey Mashayekhi, For Tech Companies Going Public, an Unwanted Side Effect: IPO-Related Lawsuits, Fortune, August 27, 2019, https://fortune.com/2019/08/27/uber-lyft-ipo-aftermath-lawsuits/; Guadalupe Gonzalez, After the Flood of IPOs? Next Come the Shareholder Lawsuits, Inc. Magazine, May 31, 2019, https://www.inc.com/guadalupe-gonzalez/ipo-shareholder-lawsuits-rising-lyft-eventbrite.html.

[2] We do not extend our study to 2020 for a few reasons. First, the Covid-19 pandemic may have caused aberrations in both IPOs and the filing of securities class actions. Second, the SPAC craze confounds counting of IPOs. Third, because there is a three-year statute of limitations for the filing of a Section 11 case, we would have to project total 2020 cases based on filings made within a short period of time following 2020 IPOs.

[3] Our approach is as follows. First, we use the Securities Data Company (SDC) Platinum database from Thomson Reuters to identify companies that went public on the NASDAQ and NYSE from 2010 to 2019. Second, for each company that went public, we searched the SSLA database for three years following the company’s IPO to see if the company was a defendant in a securities class action. Third, for each such company, we confirmed that the securities class action was based on the offering documents issued in connection with the company’s IPO.

[4] Cyan, Inc. v. Beaver Cty. Emps. Ret. Fund, 583 U.S. ___, 138 S. Ct. 1061, 200 L.Ed.2d 332 (2018).

[5] Michael Klausner, Jason Hegland, Carin LeVine & Jessica Shin, State Section 11 Litigation in the Post-Cyan Environment (Despite Sciabacucchi), 75 The Business Lawyer 1769 (2020)

[6] For example, Rey Mashayekhi’s article in Fortune states that there were 44 IPO-related cases in 2018, based on ISS data. This figure includes state and federal cases and counts parallel pairs as separate cases. Combining parallel class actions against the same IPO into one, there were 34 IPO-related cases. So, it is not the case that 44 IPOs were targeted.

[7] Sciabacucchi has since blunted Cyan’s impact on state-filed actions, by recognizing the validity of federal forum selection clauses in corporate charters. Post-Sciabacucchi state court filings volume is roughly 25% of pre-Sciabacucchi levels. Salzberg v. Sciabacucchi, 227 A.3d 102 (Del. 2020)

[8] We take the historical percentage of lawsuits filed each quarter following an IPO to project how many lawsuits will eventually be filed. For example, companies that went public in the second quarter of 2019 have had 13 lawsuits in five quarters following their IPOs. Historically, 74% of IPO lawsuits come within 5 quarters of an IPO. We therefore assume that those 13 lawsuits account for 74% of eventual lawsuits targeting IPOs in the second quarter of 2019. Hence, we project that 18 of second quarter IPOs will be targets of lawsuits. Using the same approach, we project 4 cases for first quarter IPOs, 8 cases for third quarter IPOs and 6 cases for fourth quarter IPOs—for a total of 36 cases targeting 2019 IPOs. This could be an underestimate due to a slowdown in lawsuits in 2020.

[9] This increase in lawsuits targeting IPOs might be even more pronounced if not for COVID-19. Based on filing volume prior to the pandemic, we would have projected that 26% of 2019 IPOs would eventually be targeted with litigation. However, relative to the 12-month period before the global pandemic began, total securities class action filings dropped 20% and ’33 Act cases against IPOs dropped by 50% during COVID-19.

[10] Section 11(e) of the Securities Act of 1933 provides that “[t]he suit authorized under subsection (a) may be to recover such damages as shall represent the difference between the amount paid for the security (not exceeding the price at which the security was offered to the public) and (1) the value thereof as of the time such suit was brought, or (2) the price at which such security shall have been disposed of in the market before suit… .”

[11] This excludes SPACs, closed-end funds, Real Estate Investment Trusts, Federal Banks, commercial banks, credit unions, and foreign banks. We include common stock, units, and American Depository Receipts listed on the NYSE and NASDAQ exchanges only.

[12] This excludes cases based on IPOs, Section 11 and 12 cases based on secondary offerings, and M&A objection suits.

[13] We omit from the set of already-public companies those that went public within three years, since those are among the IPO group.

[14] For the purpose of this analysis, a stock drop is considered to be connected with a 10(b) lawsuit if it falls within the class period of a 10(b) claim.

[15] All comparisons of damages and settlements are controlled for company size. 10(b) cases are limited to those against companies with market capitalizations within the first and third quartiles of market capitalization among IPOs.