The following guest post examines the resolution of class certification motions in securities class action lawsuits during 2025; considers the parties’ economic arguments in support of or in opposition to class certification; and analyzes the courts evaluation of those arguments. The article is written by Andrew Roper, Mame Maloney, Brendan Rudolph, and Ravi Sinha, Principals at The Brattle Group, and Aidan Kutner, an Associate at The Brattle Group. We would like to thank the authors for allowing us to publish their article as a guest post on our site. Here is the authors’ article.

****************************

Disclaimer: Contributing author Andrew Roper provided expert testimony in one of the matters discussed, Daniel Borteanu, et al. v. Nikola Corporation, et al. (D. Ariz. 2025). This article is descriptive in nature and does not advocate for any party’s position in that or any other case.

A valuable opportunity arises whenever defendants challenge class certification in a federal securities class action and a district court issues an order granting or denying class certification, in whole or in part, outside the context of a settlement agreement. These challenges – and the courts’ responses – provide a window into how parties present economic arguments in support of or in opposition to class certification, and how courts evaluate those arguments.

A recent report by economists from The Brattle Group (the “Brattle Report”) provides a systematic review of class certification rulings in 2025, examining the 18 federal district court orders decided outside the context of settlement (the “2025 Class Certification Orders”). The report additionally discusses defendants’ petitions to appeal these orders under Rule 23(f) in eight of the 18 cases, as well as defendants’ appeals in four other matters in which federal appellate courts issued orders in 2025. These decisions reflect how district courts evaluated defendants’ challenges to Rule 23(b)(3) in granting or denying (in whole or in part) plaintiffs’ proposed classes of investors.[ii] The sample of cases captures the views of a broad set of participants spanning multiple geographies, courts, law firms, and experts.

The analysis identifies the arguments underlying defendants’ challenges to predominance under Rule 23(b)(3) and the ways in which courts evaluated these arguments. In doing so, it provides a unique vantage point to understand 2025 jurisprudence on class certification in securities litigation. The report does not take a position on the strengths or weaknesses of any particular cases, nor does it attempt to analyze the legal or economic merits of any rulings; rather, it provides a descriptive account.

From this vantage point, the report documents how multiple defendants challenged predominance for reliance and damages using similar arguments. Multiple defendants challenged the applicability of the fraud-on-the-market presumption of reliance by attempting to rebut the three prerequisites of the theory itself: the truth is not on the market, the market is efficient, and the fraud had a price impact. Multiple defendants also argued that plaintiffs failed to specify how they could measure the inflation caused by the alleged fraud.

The report further examines how different district courts evaluated these recurring arguments. Four themes emerge from the analysis, reflecting both the types of arguments defendants are advancing and the varying ways courts respond to them. Across these themes, defendants’ challenges asked courts to evaluate case-specific public information to determine whether classwide methods of proof could be applied:

- Theme #1: Some district courts engaged with defendants’ truth-on-the-market arguments, while other courts deferred adjudication to the merits.

- Theme #2: District courts did not deny or limit class certification on the basis of challenges to market efficiency, even when defendants put forward an affirmative argument that markets were inefficient.

- Theme #3: District courts examined price impact, but the only arguments that prevailed were those following the mismatch framework set out in Goldman Sachs Grp., Inc. v. Ark. Tchr. Ret. Sys. (“Goldman ATRS”).[iii]

- Theme #4: District courts consistently held that the out-of-pocket formula could be used, finding that challenges regarding how inflation would be estimated were either unconvincing or could be resolved at trial. Importantly, 2025 also saw appellate court orders that may affect district courts’ examinations of damages going forward.

In the remainder of this article, we first provide an overview of the orders analyzed and the outcomes of these orders. We then elaborate on each of the four themes outlined above. Finally, we provide concluding thoughts and a look ahead, predicting that some of the issues challenged by defendants but deferred by district courts may resurface in the merits phase.

Across these four themes, defendants raised challenges that ultimately bear on plaintiffs’ ability to measure harm as alleged. Some of these challenges were evaluated directly by district courts, while others were deferred to the merits, either explicitly or implicitly. The Sixth Circuit’s appellate ruling in In re FirstEnergy Corp. Securities Litigation (“FirstEnergy”),[iv] which overturned class certification and remanded the district court to perform a rigorous analysis of damages as required under Comcast Corp. v. Behrend (“Comcast”),[v] demonstrates at least one circuit’s preference for addressing more of these challenges at the class certification stage. Challenges that do not ultimately lead courts to impose a barrier to class certification may resurface in the merits phase and/or affect the settlement posture.

Class Certification Outcomes in 2025

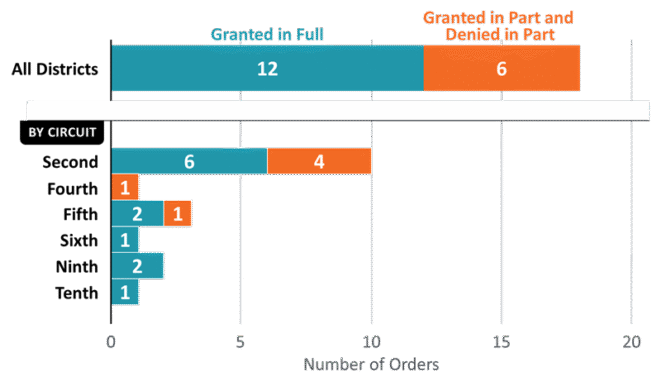

In 2025, there were 18 class certification orders issued by federal district courts in which the court either granted or denied (in whole or in part) plaintiffs’ proposed classes of investors.[vi]

Figure 1 below summarizes the judicial outcomes of these 2025 class certification orders: In 12 of 18 cases, federal district courts granted certification in full. [vii] In the remaining six of 18 cases, certification was granted in part and denied in part. These partial denials of certification occurred across three different federal district circuits: the Second, Fourth, and Fifth.

In all six of these cases, defendants argued that plaintiffs had failed to satisfy Rule 23(b)(3)’s predominance requirement with respect to reliance. The courts agreed in part and limited the certified class on this basis.[viii] In three of these cases, defendants further argued that plaintiffs failed to satisfy Rule 23(b)(3)’s predominance requirement with respect to damages, but the courts rejected these challenges.

Figure 1: Judicial Outcomes of the 2025 Class Certification Orders

In the six cases in which the courts denied certification in part, the outcomes were as follows:

- Truth-on-the-Market. The district courts in In re The Boeing Company Securities Litigation (“Boeing”)[ix] and In re National Instruments Corporation Securities Litigation (“National Instruments”)[x] granted certification to a shorter class periodthan was proposed because predominance could not be satisfied for reliance because the truth was on the market.

- Price Impact Rebuttal. The district courts in Plaut v. The Goldman Sachs Group, Inc. et al. (“Goldman 1MDB”),[xi] City of Warwick Retirement System v. Concho Resources Inc. et al. (“Concho”),[xii] and Boeing denied certification in part because defendants rebutted price impact for some, but not all, of the alleged material misrepresentations. In these matters, the district courts excluded certain alleged material misrepresentations, ruling that the fraud-on-the-market theory did not apply to those statements.

- Affiliated Ute Challenge. The district court in In re DiDi Global Inc. Securities Litigation (“DiDi”)[xiii] denied certification in part, ruling that plaintiffs were not entitled to the presumption of reliance under Affiliated Ute under Section 10(b) for a subset of allegations (but holding that Affiliated Ute could still be applied for other allegations).

- Conflict Between Subclasses. The district court inChahal v. Credit Suisse Group AG et al. (“Credit Suisse XIV”)[xiv] denied certification to one of two proposed subclasses, ruling that there was a “fundamental conflict” between “the classes’ theories of liability.”

Theme #1: Truth-on-the-Market Challenges

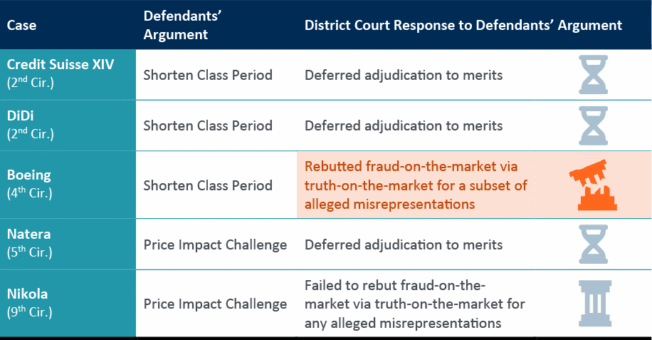

In five of the 2025 class certification orders (Credit Suisse XIV, Boeing, DiDi, Natera, and Nikola), defendants challenged the applicability of the fraud-on-the-market theory in matters where publicly available information had corrected (or revealed) some or all of the allegedly misrepresented (or omitted) material facts. Defendants’ truth-on-the-market challenges examined the first prerequisite of the fraud-on-the-market theory: that the truth is not on the market.

In these challenges, some defendants argued that the proposed class period should be shortened after the truth was on the market. Other defendants made further arguments that price impact could be rebutted because the truth was on the market.

Different courts expressed different preferences for adjudicating truth-on-the-market challenges raised by defendants. In two cases (Boeing and Nikola), the district court engaged with the information that the defendants argued was available to investors, and in Boeing, the district court limited the class period on this basis. In the other three instances, district courts stated that these economic arguments could not be evaluated at the class certification stage, because similar analyses may also be examined in the merits stage as part of the materiality inquiry. Figure 2 below summarizes the Brattle Report’s findings.

Figure 2 summary of defendants’ Truth-on-the-Market challenges and district court responses

Note: Orange shading indicates cases in which the district court agreed (in part) with defendants’ truth-on-the-market challenges and limited the certified class on that basis.

Theme #2: Market Efficiency Challenges

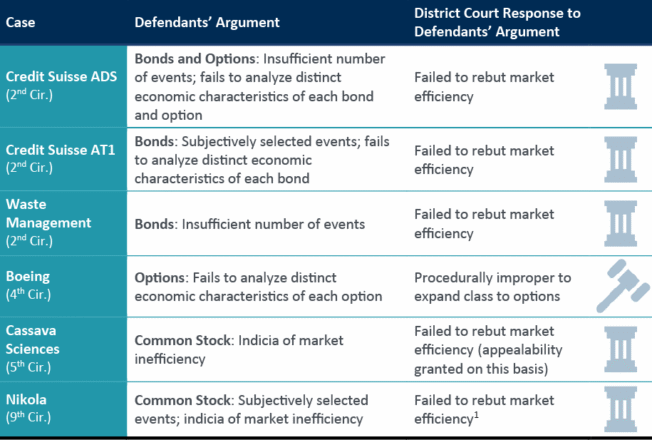

In six of the 2025 class certification orders (Credit Suisse ADS, Credit Suisse AT1, Waste Management, Boeing, Cassava, and Nikola), defendants challenged whether plaintiffs had demonstrated market efficiency. These challenges to market efficiency examined the second prerequisite of the fraud-on-the-market theory: public information is rapidly and fully reflected in the price through market efficiency.

Specifically, across four matters involving debt, notes, or options, defendants challenged the analyses put forward by plaintiffs to establish market efficiency. In these instances, defendants raised similar methodological challenges. Separately, in two instances involving common stock (Cassava Sciences and Nikola), defendants went further by arguing that the case facts indicated that the market was inefficient.

No district court in the 2025 class certification orders denied or limited class certification on the basis that plaintiffs failed to establish market efficiency. However, in Cassava Sciences, the court of appeals for the Fifth Circuit granted the defendants’ petition for permission to appeal based, in part, on the district court’s opinion on market efficiency. Figure 3 below summarizes the Brattle Report’s findings.

Figure 3: summary of defendants’ challenges to market efficiency and district court responses

Theme #3: Price Impact Challenges

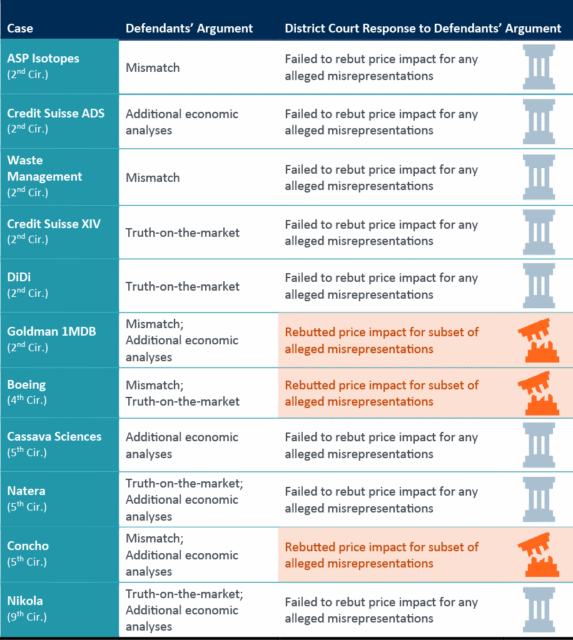

In 11 of the 18 2025 class certification orders, defendants argued they had rebutted price impact for some or all of the alleged material misrepresentations. These rebuttals of price impact follow Halliburton II’s invitation to explore the third prerequisite of the fraud-on-the-market theory: the alleged material misrepresentation impacted the price.[xvi]

In some cases, defendants argued that there was an informational mismatch between the alleged material misrepresentations and the alleged corrective disclosures that ruled out price impact following Goldman ATRS. In some cases, defendants described how their testifying experts performed economic analyses purportedly rebutting price impact.

In three matters (Goldman 1MDB, Boeing, and Concho), district courts denied certification in part on the basis that defendants had successfully rebutted price impact. In these instances, the district courts denied certification because of an information mismatch following Goldman ATRS. While district courts engaged with the other types of economic analyses presented, they were either unpersuaded by the arguments or determined that the argument should be held over for trial. Figure 4 below summarizes the Brattle Report’s findings.

In addition, the Third Circuit (in Hall v. Johnson & Johnson et al.) and Ninth Circuit (in Jaeger v. Zillow Group Inc. et al.) affirmed district court orders granting certification, which had been appealed by defendants on the basis of price impact. In Oklahoma Firefighters Pension and Retirement System v. Biogen Inc. et al., the First Circuit denied appealability of a similar price impact challenge.[xvii]

Figure 4: summary of defendants’ challenges to price impact and district courts’ responses

Note: Orange shading indicates cases in which the district court agreed (in part) with defendants’ challenges to price impact and limited the certified class on that basis.

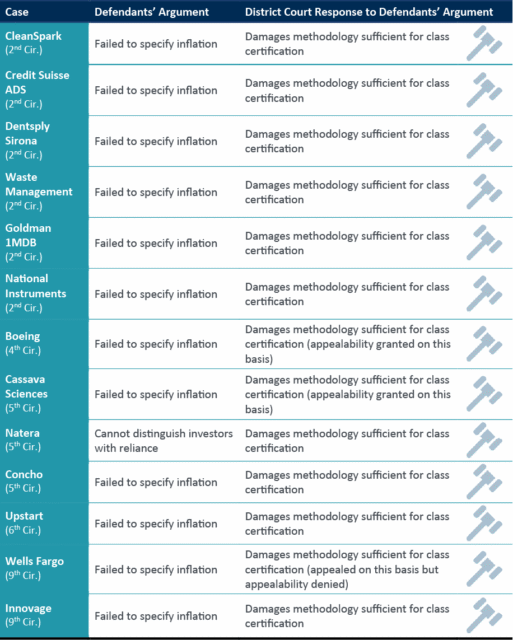

Theme #4: Damages Challenges

In 13 of the 18 2025 class certification orders, defendants challenged whether plaintiffs had successfully established that damages are calculable on a classwide basis, as required for predominance under Rule 23(b)(3). In most of these challenges, defendants questioned whether plaintiffs had specified how they intended to measure inflation to calculate damages using the out-of-pocket formula. However, in none of these 13 matters did the district courts deny or limit class certification on the basis of those criticisms. Figure 5 summarizes the Brattle Report’s findings.

Importantly, in contrast to these district court decisions, a Sixth Circuit court of appeals order in In re FirstEnergy Corp. Securities Litigation (“FirstEnergy”)[xviii] overturned class certification and remanded the district court to perform a rigorous analysis of damages as required under Comcast Corp. v. Behrend (“Comcast”).[xix] Further, the Fourth Circuit (in Boeing) and Fifth Circuit (in Cassava Sciences) both granted review to consider the sufficiency of plaintiffs’ showing of damages under Comcast. However, a similar challenge was denied review in the Ninth Circuit (in Wells Fargo).

Figure 5: summary of defendants’ challenges to damages and district courts’ responses

Concluding Thoughts and Looking Ahead

The Brattle Report documents how multiple defendants in securities class actions argued that case-specific facts – publicly available to both defendants and plaintiffs without discovery – undermined the applicability of the fraud-on-the-market theory by showing that its required predicates are not satisfied. The report also describes how multiple defendants contended that case-specific facts and circumstances suggest that inflation cannot be reliably estimated across the class period, as required by the out-of-pocket formula for damages proposed by plaintiffs.

Each of these challenges asked a district court to evaluate the case-specific fact pattern of public disclosures and additional sources of public information to determine the applicability of the fraud-on-the-market theory or out-of-pocket damages formula at the time of class certification.

Overall, our analysis of jurisprudence related to the 2025 class certification orders indicates that district courts have taken differing approaches to whether such challenges can be fully evaluated at class certification. In some instances, courts evaluated the case-specific fact patterns and reached a determination. In others, courts stated that they were precluded from evaluating these case-specific fact patterns. In at least one case (DiDi), the court determined that adjudication of the issue should be reserved for the merits, even if the argument was persuasive at class certification.

Ultimately, these challenges bear on plaintiffs’ ability to measure harm as alleged. Under the fraud-on-the-market theory, the alleged harm is caused by the price impact of the alleged misrepresentations. By examining the total mix of information, defendants seek to rebut the presumption of price impact, which in turn affects whether inflation can be measured as an input to the out-of-pocket formula.

Accordingly, district courts may increasingly be required to engage with these arguments at the class certification stage – particularly in light of the Sixth Circuit’s decision in FirstEnergy, which reminded courts of their potential obligations under Comcast, as well as the Fourth and Fifth Circuits’ orders granting review of these issues in Boeing and Cassava Sciences.

Looking ahead, the extent to which courts engage with these arguments at the class certification stage – rather than deferring them to the merits – may shape both litigation strategy and the practical viability of classwide proof in securities cases.

A more detailed analysis of these findings is available in the full Brattle Report, which can be found on Brattle’s website here.

Andrew Roper, Mame Maloney, Brendan Rudolph, and Ravi Sinha are all Principals, and Aidan Kutner is an Associate, at The Brattle Group. Dr. Roper and Mr. Sinha are Co-Leaders of the firm’s Securities Class Actions practice, and Mr. Rudolph is the Co-Leader of the Private Equity, Venture Capital & Hedge Funds practice.

[ii] In these matters, plaintiffs proposed damage classes for investors who purchased or acquired publicly traded stock, debt, notes, or options for alleged violations under Section 10(b) of the Exchange Act of 1934.

[iii] Goldman Sachs Grp., Inc. v. Ark. Tchr. Ret. Sys., 594 US 113, 123 (2021) (explaining that price impact inference “starts to break down when there is a mismatch between the contents of the misrepresentation and the corrective disclosure.”); Ark. Tchr. Ret. Sys. v. Goldman Sachs Grp., Inc., 77 F.4th 74, 80 (2d Cir. 2023) (“the back-end price drop—what happens when the truth is finally disclosed—operates as an indirect proxy for the front-end inflation, or the amount that the misrepresentation fraudulently propped up the stock price.”).

[iv] In re FirstEnergy Corp. Securities Litigation, 149 F.4th 587 (6th Cir. 2025).

[v] Comcast Corp. v. Behrend, 569 U.S. 27 (2013).

[vi] In these matters, plaintiffs petitioned damage classes for investors who purchased or acquired publicly traded stock, debt, notes, or options for alleged violations under Section 10(b) of the Exchange Act of 1934.

[vii] Leone v. ASP Isotopes Inc., et al., No. 1:24-cv-9253-CM (S.D.N.Y., December 4, 2025) (“ASP Isotopes”); Darshan v. CleanSpark, Inc., et al., No. 1:21-cv-00511-LAP (S.D.N.Y., September 24, 2025) (“CleanSpark”); In re Credit Suisse Securities Class Actions, No. 1:23-cv-5874-CM-SLC (S.D.N.Y., July 7, 2025) (“Credit Suisse ADS”); Core Capital Partners, Ltd. v. Credit Suisse Group AG et al., No. 1:23-cv-9287-CM (S.D.N.Y., November 13, 2025) (“Credit Suisse AT1”); San Antonio Fire and Police Pension Fund, et al., v. Dentsply Sirona Inc., et al., No. 22-cv-06339-AS (S.D.N.Y., July 10, 2025) (“Dentsply Sirona”); In re Waste Management Securities Litigation, No. 1:22-cv-04838-LGS (S.D.N.Y., March 31, 2025) (“Waste Management”); In re Cassava Sciences Inc. Securities Litigation, No. 1:21-cv-00751-DAE (W.D. Tex., August 12, 2025) (“Cassava Sciences”); Schneider v. Natera, Inc., et al., No. 1:22-cv-00398-DAE (W.D. Tex., March 21, 2025) (“Natera”); Crain v. Upstart Holdings, Inc. et al., No. 2:22-cv-02935-ALM-EPD, (S.D. Ohio March 27, 2025) (“Upstart”); Borteanu v. Nikola Corporation et al., No. 2:20-cv-01797-SPL (D. Ariz. January 6, 2025) (“Nikola”); SEB Investment Management AB et al. v. Wells Fargo & Company et al., No. 3:22-cv-03811-TLT (N.D. Cal. April 25, 2025) (“Wells Fargo”); McLeod v. Innovage Holding Corp. et al., No. 1:21-cv-02770-WJM-SBP (D. Colo. January 8, 2025) (“Innovage”).

[viii] In one of these six cases – Credit Suisse XIV – defendants challenged predominance for reliance as well as adequacy of the lead plaintiffs. Credit Suisse XIV 2023 Opposition Motion pp. 15, 21. The court in this matter denied class certification in part on the basis of adequacy.

[ix] In re The Boeing Company Securities Litigation, No. 1:24-cv-151-LMB-LRV (E.D. Va., March 7, 2025).

[x] In re National Instruments Corporation Securities Litigation, No. 1:23-cv-10488-DLC (S.D.N.Y., September 19, 2025).

[xi] Plaut v. The Goldman Sachs Group, Inc. et al., No. 1:18-cv-12084-VSB-KHP, (S.D.N.Y., September 4, 2025).

[xii] City of Warwick Retirement System v. Concho Resources Inc. et al., No. 4:21-cv-02473, (S.D. Tex. April 7, 2025).

[xiii] In re DiDi Global Inc. Securities Litigation, No. 1:21-cv-05807-LAK-VF (S.D.N.Y., August 13, 2025).

[xiv] Chahal v. Credit Suisse Group AG et al., No. 1:18-cv-02268-AT-SN (S.D.N.Y., February 11, 2025).

[xv] The district court also stated that while the plaintiffs’ expert analysis may not have been perfect, it could still be challenged at trial. Nikola Order p. 21. (“Furthermore, Defendants’ continued attempts to couch their disagreements with the findings of [plaintiffs’ expert] event study as methodological criticisms are unavailing for the purposes of their Motion to Exclude his proposed opinions and testimony. … Plaintiffs also adequately address each of Defendants’ claimed “fatal flaws” in Dr. Nye’s study. As to Dr. Nye’s selection of event dates, Plaintiffs note that the events were defined “ex ante . . . as the Company’s quarterly and year-end earnings announcements,” which is a methodology “supported by the literature” and regularly employed by experts. (Doc. 200 at 10). Here, as in other cases, the Court agrees that “[w]hile Dr. Nye’s study may not be perfect, it is not unreliable. Defendants may challenge Dr. Nye’s conclusions in the appropriate forum, that is, at trial.”

[xvi] Halliburton Co. v. Erica P. John Fund, Inc., 573 US 258 (2014) (“Halliburton II”).

[xvii] Hall v. Johnson & Johnson et al., No. 3:18-cv-01833-ZNQ-TJB (3d Cir., October 15, 2025) (“Johnson & Johnson”); Jaeger v. Zillow Group Inc et al., No. 2:21-cv-01551-TSZ (9th Cir., September 26, 2025) (“Zillow”).

[xviii] In re FirstEnergy Corp. Securities Litigation (6th Cir. August 13, 2025).

[xix] Comcast Corp. v. Behrend, No. 11-864, March 27, 2013.